You have heard it a hundred times: you need a budget. But most budgeting methods feel like punishment. Spreadsheets, categories for every tiny purchase, guilt every time you buy coffee. No wonder people give up after two weeks.

The 50/30/20 rule is different. It is simple, flexible, and it actually works for normal people with normal lives. Senator Elizabeth Warren popularized it in her book All Your Worth, and it has since become one of the most recommended budgeting frameworks by financial experts worldwide.

Here is exactly how it works and how you can start using it today.

What Is the 50/30/20 Rule?

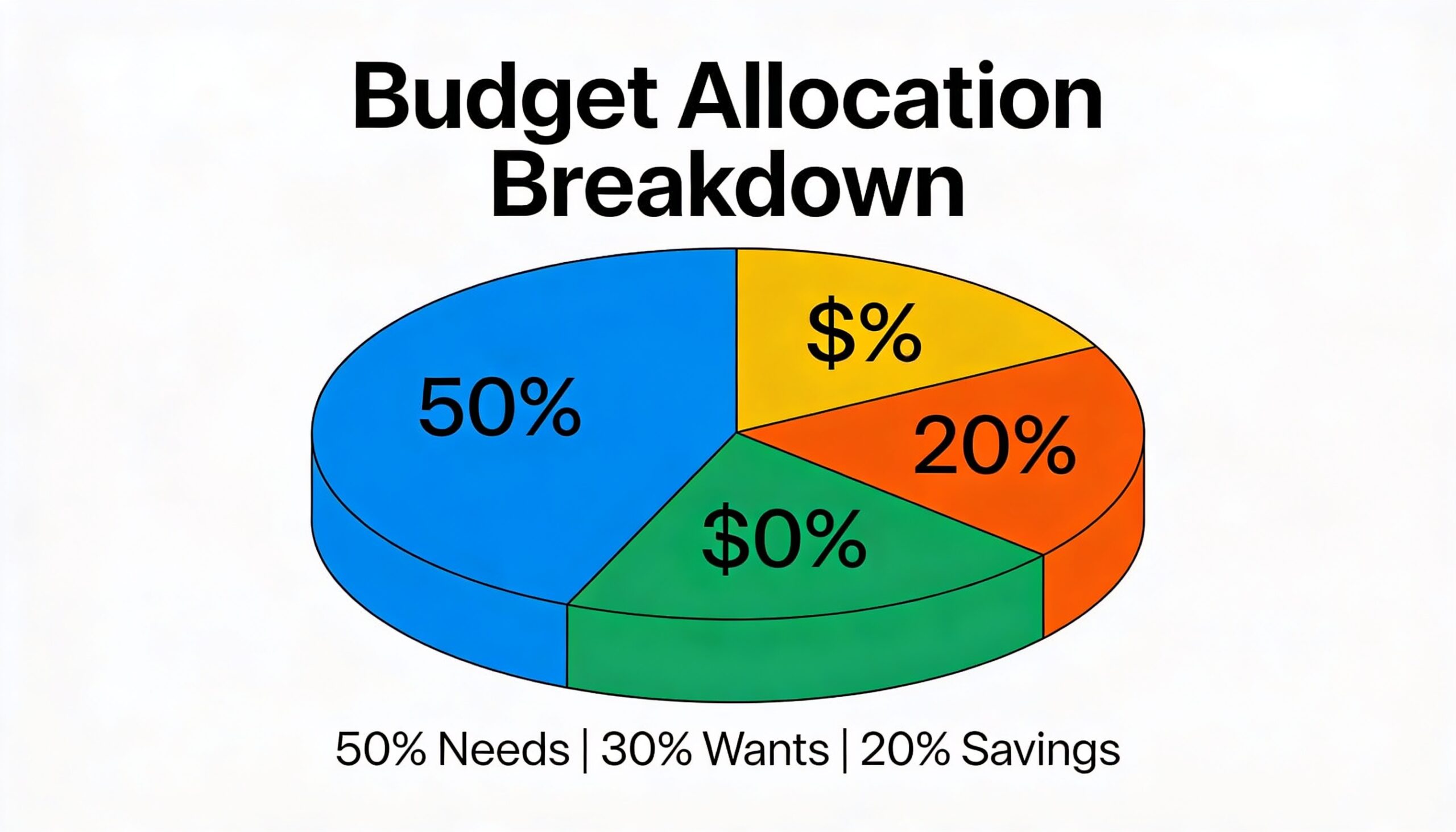

The 50/30/20 rule divides your after-tax income into three buckets:

- 50% for Needs — essentials you cannot avoid

- 30% for Wants — things that make life enjoyable

- 20% for Savings and Debt — building your financial future

That is it. Three categories. No tracking every single dollar. Just a clear framework that keeps you on track without making you miserable.

The 50% — Your Needs

Half of your take-home pay goes to things you genuinely cannot live without. These are the non-negotiable expenses:

- Rent or mortgage payments

- Utilities (electricity, water, gas, internet)

- Groceries (not dining out — that is a want)

- Health insurance and medical costs

- Minimum debt payments

- Transportation (car payment, gas, public transit)

- Basic phone plan

The key test: If you would face serious consequences for not paying it, it is a need. If life would just be less fun without it, it is a want.

What If Your Needs Exceed 50%?

If you live in an expensive city, your rent alone might eat up 40% of your income. That is okay — the 50/30/20 rule is a guideline, not a law. But it does signal that you should look for ways to reduce those costs over time. Consider:

- Getting a roommate to split rent

- Refinancing your mortgage or car loan

- Switching to a cheaper phone plan

- Shopping at discount grocery stores

- Negotiating your insurance rates

The 30% — Your Wants

This is the part most budgets skip, and it is exactly why those budgets fail. You are a human being, not a savings robot. The 30% for wants is what makes this budget sustainable long-term.

Wants include:

- Dining out and takeout

- Streaming subscriptions (Netflix, Spotify, etc.)

- Shopping for clothes beyond basics

- Hobbies and entertainment

- Vacations and travel

- Gym membership

- The fancy coffee you love

Important: Wants are not bad. Spending money on things you enjoy is part of a healthy financial life. The 50/30/20 rule just makes sure you do it within a sustainable boundary.

The 20% — Savings and Debt Repayment

This is where you build real wealth. The last 20% goes toward your financial future:

- Emergency fund — aim for 3 to 6 months of expenses

- Retirement accounts — 401(k), IRA, or pension contributions

- Extra debt payments — anything above the minimum payment

- Investments — index funds, stocks, or other assets

- Savings goals — house down payment, car fund, education

Priority Order for Your 20%

- Build a starter emergency fund — at least $1,000 to cover unexpected expenses

- Pay off high-interest debt — credit cards and personal loans first

- Grow your emergency fund — up to 3 to 6 months of expenses

- Invest for retirement — take advantage of employer matching if available

- Save for other goals — house, education, or anything else you want

Real Example: The 50/30/20 Rule in Action

Let us say you bring home $4,000 per month after taxes. Here is how your budget would look:

- Needs (50%): $2,000 — Rent $1,200, utilities $200, groceries $300, insurance $150, transportation $150

- Wants (30%): $1,200 — Dining out $200, entertainment $150, subscriptions $50, shopping $200, hobbies $100, miscellaneous $500

- Savings (20%): $800 — Emergency fund $200, retirement contribution $400, extra debt payment $200

Simple, right? You are not tracking whether you spent $4.50 or $5.00 on coffee. You are just making sure each bucket stays roughly where it should be.

How to Start the 50/30/20 Budget Today

Step 1: Calculate Your After-Tax Income

Look at your paycheck — the amount deposited in your bank account is your after-tax income. If you freelance or have irregular income, use the average of the last three months.

Step 2: List Your Needs

Go through your bank statements and identify every essential expense. Be honest — Netflix is not a need, even if it feels like one.

Step 3: Set Up Automatic Savings

Before you spend anything on wants, set up an automatic transfer for 20% on payday. Pay yourself first. What you do not see, you do not spend.

Step 4: Spend the Rest Guilt-Free

Whatever is left after needs and savings is your wants budget. Spend it however you like — you have already taken care of the important stuff.

Common Mistakes to Avoid

- Confusing wants with needs. A car might be a need. A brand-new BMW is a want with a need hiding inside it.

- Being too strict. If you never allow yourself any wants, you will burn out and abandon the budget entirely.

- Ignoring irregular expenses. Annual subscriptions, car maintenance, and holiday gifts count too. Divide them by 12 and include them monthly.

- Not adjusting over time. Got a raise? Increase your savings percentage. Income dropped? Temporarily reduce wants. The budget should flex with your life.

Who Is the 50/30/20 Rule Best For?

This budgeting method works best for:

- Beginners who find detailed budgets overwhelming

- Steady income earners with predictable paychecks

- People who hate tracking every purchase

- Anyone who has tried and failed with other budgeting methods

It may not be ideal if you have very high debt (you might want 30% or more going to debt repayment) or very low income (your needs may exceed 50%). In those cases, adjust the percentages to fit your situation — the principle still applies.

The Bottom Line

The 50/30/20 rule is not about perfection. It is about direction. As long as you are roughly following the framework, you are ahead of most people who have no plan at all.

Start this month. Calculate your numbers, set up automatic savings, and give yourself permission to enjoy the wants category. Your future self will thank you.

2 Comments on “50/30/20 Rule Explained: A Simple Budget That Actually Works”